The illusion of plenty ends in September

The illusion of plenty ends the same way every great oil shock has ended: at the moment when the buffer everyone assumed would appear on command turns out to have been a historical accident, a political subsidy or a logistical trick that belonged to another era.

In 1973, the system still had Saudi spare capacity behind it. In 1990, after Iraq invaded Kuwait, Saudi Arabia could ramp output and replace part of the lost supply. In 2022, Russian barrels did not vanish, but moved east through discounts, shadow fleets and longer trade routes. Each crisis looked catastrophic at the headline level, yet each crisis still had a release valve. Someone could pump more, someone could reroute, someone could absorb, someone could buy time. JPMorgan’s “The Illusion of Plenty” is disturbing because 2026 no longer fits that pattern.

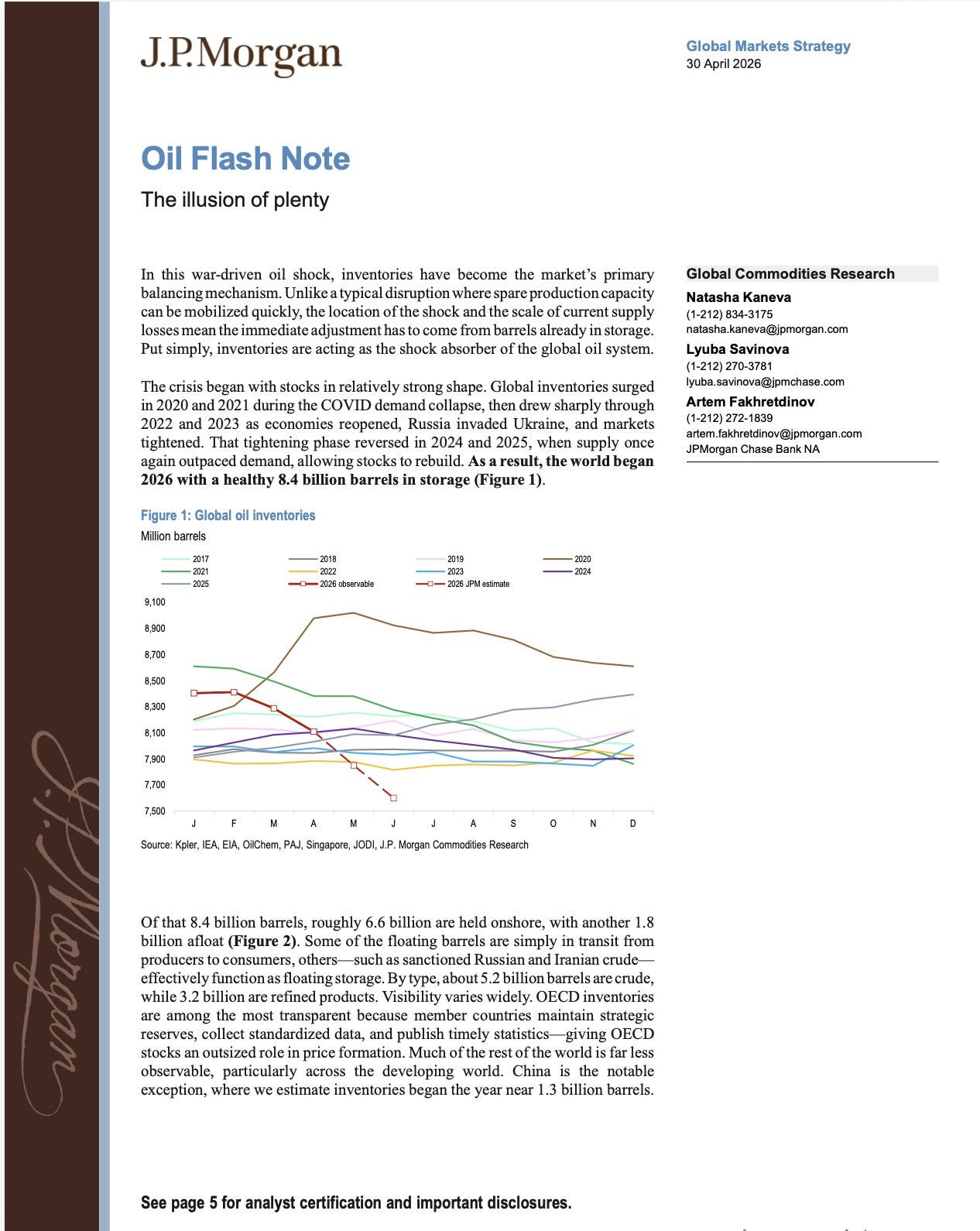

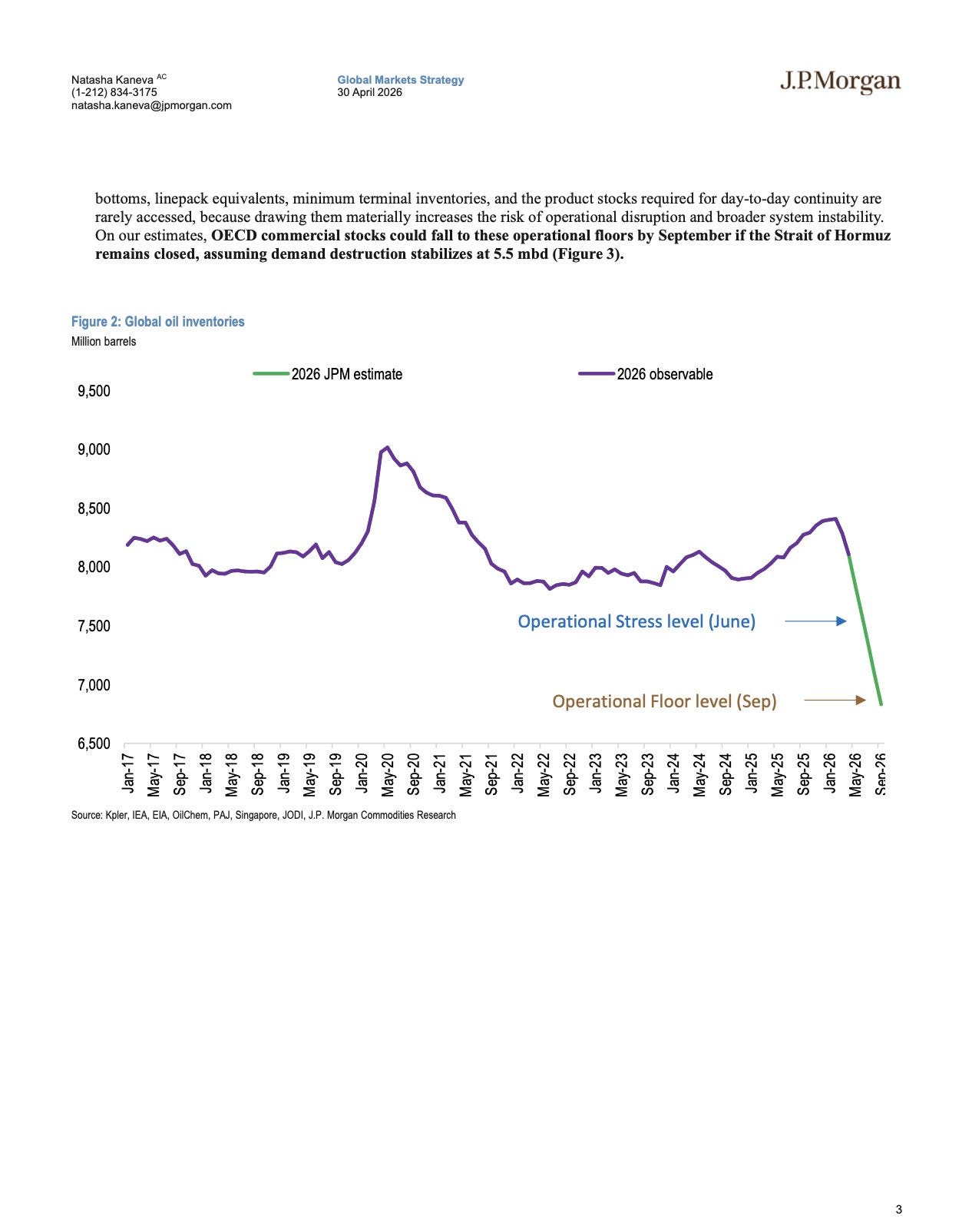

The world appears to hold 8.4 billion barrels of oil inventory, which sounds like abundance until the number is taken apart. Some barrels are pipeline fill, some are tank bottoms, some are locked in the wrong geography, some are the wrong grade for the refinery that needs them, some sit in strategic reserves that governments touch only under political stress and some float on water between producer and consumer, useful but finite. Only around 0.8 billion barrels are realistically drawable before the system approaches operational stress. The market is therefore sitting on a thin layer of movable barrels above a vast base of inventory that must remain in place so the machine can keep breathing.

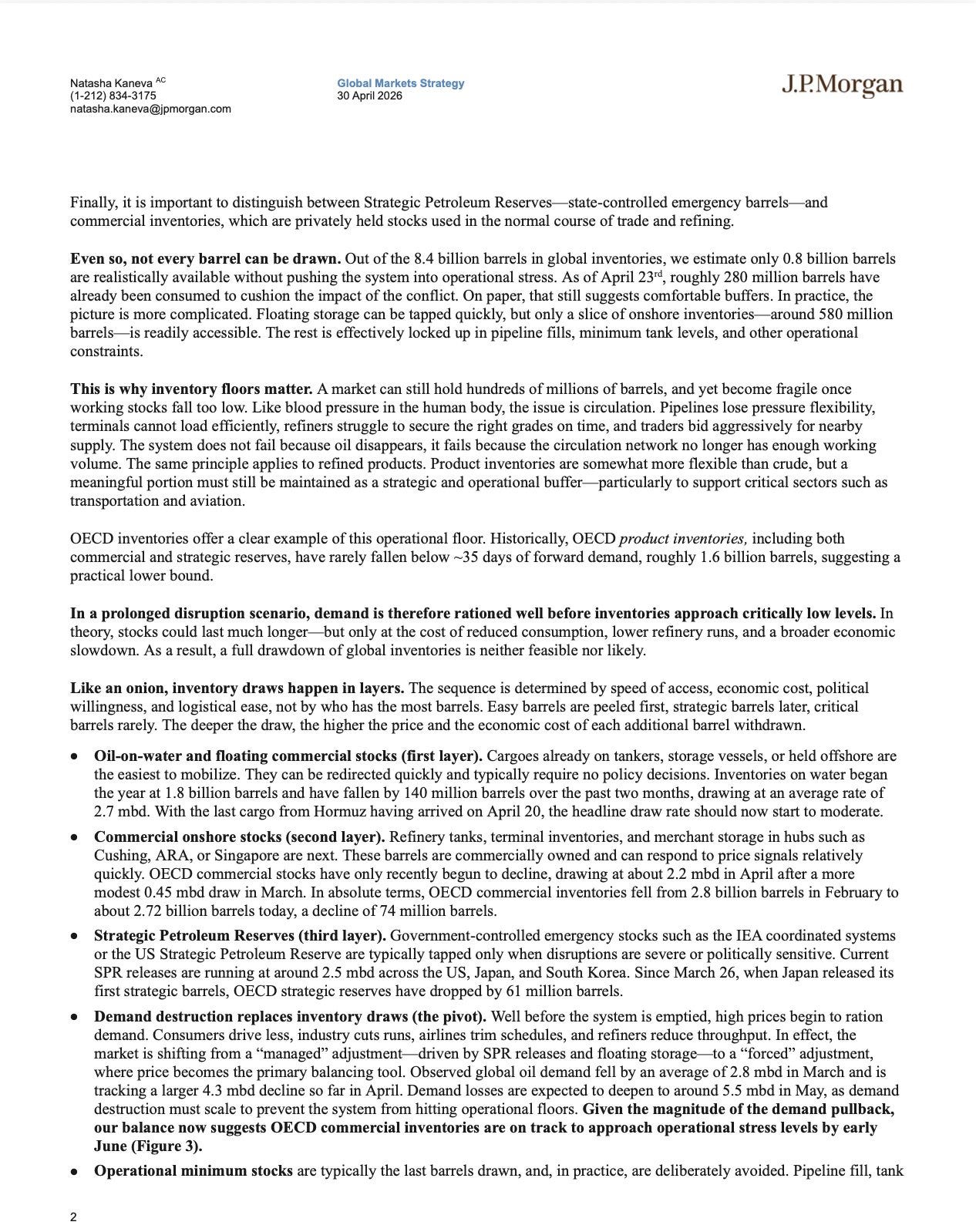

JPMorgan says global inventories could hit “Operational Floor” by September if Hormuz remains closed. The Operational Floor is the minimum inventory level required to keep the oil system alive, because pipelines need pressure, terminals need minimum stock, refineries need continuous feedstock and logistics networks need refined products moving through the chain without interruption. Once inventories fall below that level, the market is no longer dealing with an ordinary shortage, but with the first stage of cascade failure.

A cascade failure looks like a refinery shutting because the right crude no longer arrives, then product shortages appearing at terminals, then fuel rationing at petrol stations, then freight, aviation, agriculture and industrial supply chains being prioritized or curtailed, then food distribution and basic logistics becoming political questions rather than market functions. It starts with oil, but it does not end with oil, because diesel, jet fuel, petrochemicals, fertilizer inputs, trucking routes, cold chains, emergency services and supermarket shelves are all downstream expressions of the same circulation system.

That is why Hormuz changes the entire structure of the crisis. In an ordinary oil shock, inventories bridge time until spare capacity, rerouting or demand adjustment takes over. Here, spare capacity is almost gone, rerouting is constrained by geography and security and demand destruction becomes the physical rationing mechanism through which airlines cut routes, refineries reduce runs, factories slow output, governments manage fuel flows and consumers discover that price has become a gate rather than a signal. JPM describes the sequence clearly: floating storage is pulled first, OECD commercial onshore stocks draw harder next, strategic reserves enter the chain after that, while observed demand destruction has already moved from 2.8 million barrels per day in March to 4.3 million in April, with roughly 5.5 million barrels per day required in May to slow the inventory collapse.

A barrel in a strategic reserve has a different economic value from a barrel already in transit: crude is not refined product, oil in China is not oil at a European terminal, a barrel that technically exists but cannot move through the right pipe, reach the right refinery, match the right grade and arrive at the right time is no longer a buffer in any meaningful sense. Modern oil fragility begins before the last barrel is consumed, at the point where working stocks fall below the level required to maintain pipeline pressure, terminal flexibility, refinery continuity and diesel availability across logistics networks.

Government intervention then becomes the final buffer. Mandatory fuel rationing, export bans, emergency price controls, subsidy regimes and even COVID-style mobility restrictions would not arrive as elegant macro policy, but as desperate attempts to stop the physical system from seizing up. The objective would be to keep the infrastructure alive long enough for barrels, routes, refineries and demand to be forced back into some kind of workable alignment.

That is the historical break. The 1970s were an inflationary oil-price shock. 1990 was a war shock with Saudi offset. 2022 was a sanctions shock softened by rerouting. 2026, under JPM’s September scenario, becomes an inventory-floor shock, where the buffer itself is consumed and the market shifts from voluntary pricing into involuntary allocation. The optimistic reading says Hormuz reopens before September because every rational actor can see the cliff. The darker reading says governments often treat cliffs as bargaining positions until the ground disappears.