What if the AI boom goes into reverse

Simulations around a possible reversal of the AI investment boom paint a far more fragile picture than current market pricing suggests. Three scenarios were modeled: a correction of excess AI-driven capital spending, a standard recession in US technology investments and a replay of the post-2000 dot-com collapse. In every case, the damage spreads far beyond Silicon Valley, hitting European and UK markets with disproportionate force because growth there is already weak enough that even a moderate external shock could tip economies into recession.

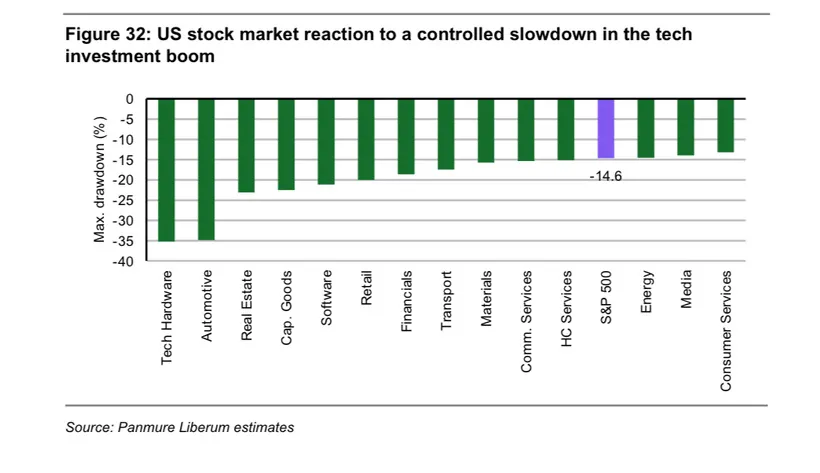

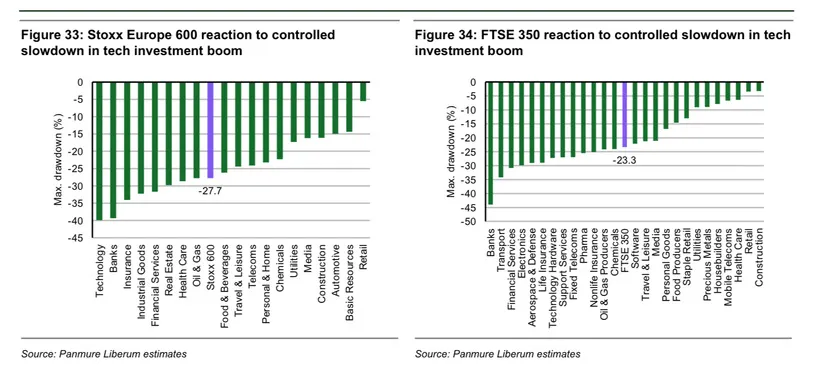

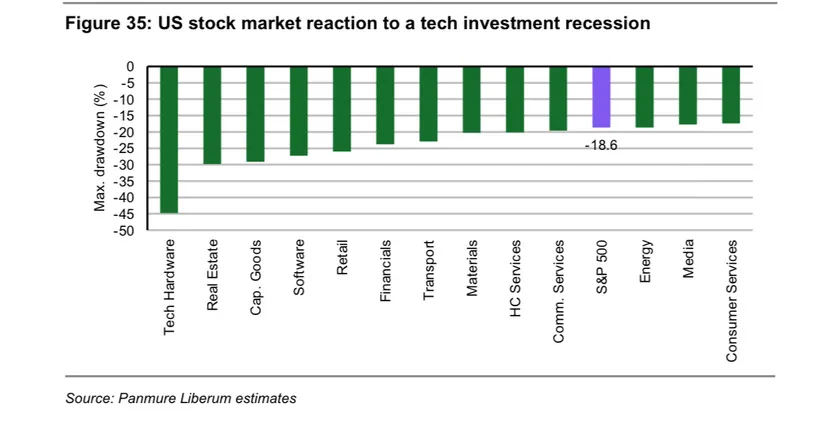

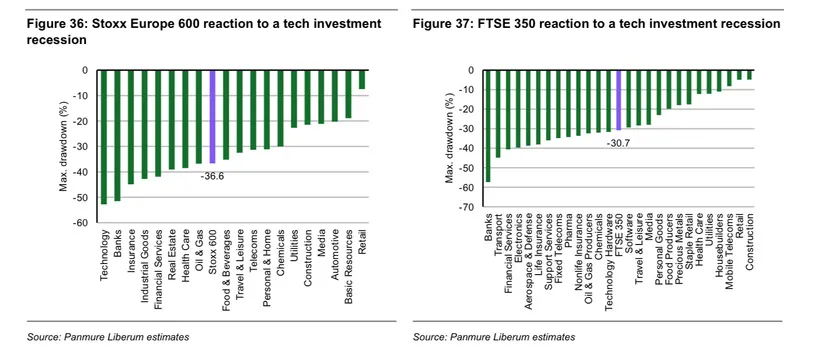

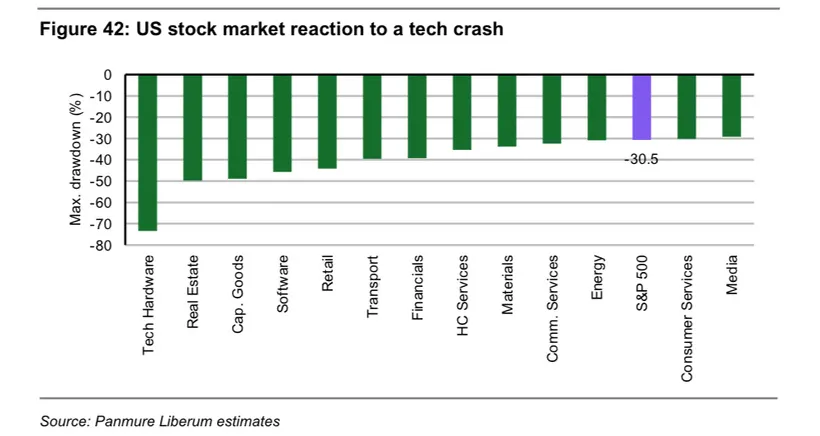

Even the mildest scenario like simply a cooling of excessive US tech investment points toward a fresh bear market in Europe and the UK. A more traditional tech recession, especially if combined with a broader US slowdown, projects roughly a 20% decline for US equities while European and British markets could fall 30% or more. The most extreme simulation, modeled on the early-2000s TMT collapse, suggests technology stocks could lose over 70% within a year, dragging the S&P 500 down more than 30%.

Experienced investors know this pattern well: when the US sneezes, the rest of the world catches a cold. European and UK markets historically suffer deeper drawdowns for two reasons. First, during periods of stress, American capital tends to flee foreign markets and return home, even when the crisis itself originated in the United States. That dynamic intensified both the dot-com collapse and the 2008 financial crisis, creating an additional layer of selling pressure across Europe. Second, Europe and the UK operate with structurally weaker growth rates, meaning that a shock which merely slows the US economy can push large parts of Europe directly into recession. Once recession risks emerge, investors usually accelerate the sell-off preemptively.

Technology stocks in Europe are projected to be among the hardest hit, with simulations indicating potential drawdowns of roughly 40%, while banks and financial services could also materially underperform as weaker growth, deteriorating credit conditions and recession fears compress profitability across the sector.

Ironically, the sectors expected to hold up best during an AI unwind are the least glamorous corners of the market: European retailers such as Inditex, H&M, Next plc and B&M, alongside UK construction names like Balfour Beatty, Morgan Sindall and Keller Group. In the simulations, these areas lose less than 10%.

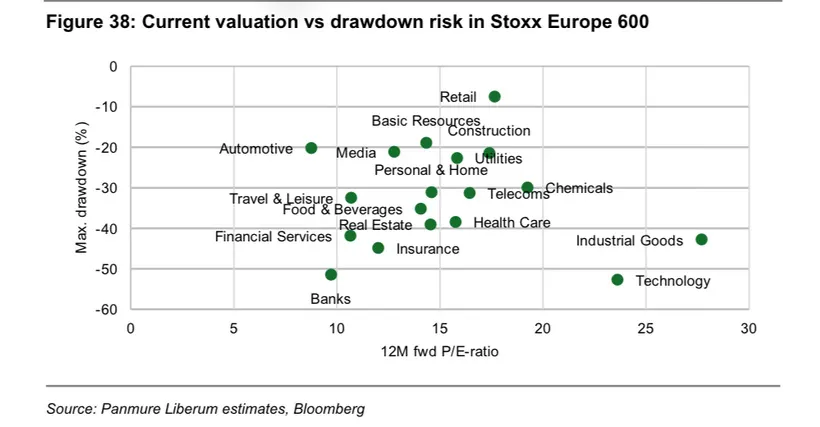

An important result to heed for investors is that low valuations are unlikely to protect against large drawdowns. Yes, European and US stocks are generally cheaper than their US peers, and some beaten-down sectors like European automotive, UK media, and travel and leisure across the UK and Europe look particularly cheap, but Fig 38 shows that there is no correlation between the current 12M forward P/E-ratios of a sector and the expected drawdown in this scenario.

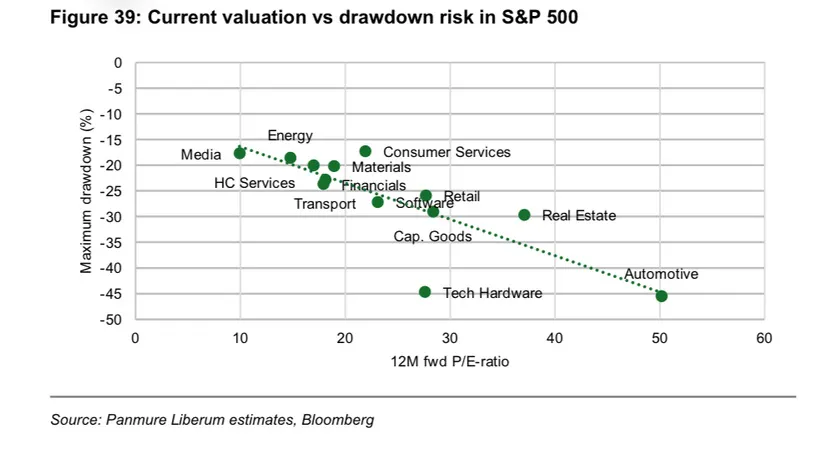

Fig 39 shows that in the US, this is rather different. There, the most expensive sectors like technology and automotive are likely to see the largest drawdowns, while cheaper sectors like healthcare services, media and energy are likely more resilient. In the US, we can thus conclude that in the case of a tech recession, value stocks should outperform growth stocks by a wide margin.

The last simulation, effectively a replay of the 2000–2003 dot-com collapse under today’s AI conditions, delivers a reminder of how violently speculative manias can unwind once capital markets stop believing the growth narrative. In this scenario, the S&P 500 is projected to lose roughly 30% within the first year alone, almost identical to the initial phase of the original TMT crash before the shock of 9/11 accelerated panic further. Technology hardware stocks would absorb the real destruction, with projected first-year losses approaching 74%, remarkably close to the collapse experienced during the early-2000s unwind when the sector ultimately lost as much as 86% from peak to trough.

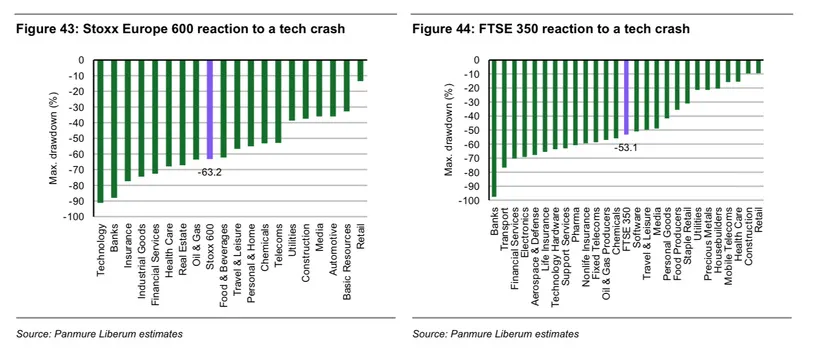

At first glance, Europe and the UK hardly look like safe places to hide. Simulations project the STOXX Europe 600 falling more than 60%, while the FTSE 350 could lose over half its value during the first year of the shock. Financials, banks, insurers and cyclical industries across Europe would likely be hit especially hard as recession fears, shrinking liquidity and collapsing investor confidence reinforce each other in classic bear-market fashion.

Yet beneath the surface, the simulations reveal an uncomfortable truth many investors ignore during speculative booms: in real crashes, boring businesses often outperform futuristic narratives. While nearly every sector in the US market is projected to lose at least 30%, several European and British companies tied to essential consumption and physical infrastructure show far greater resilience. European retailers such as Inditex, H&M and Next plc are projected to decline only modestly relative to the broader collapse.

The UK market stands out even more because of its defensive composition. Retailers like Next plc, Kingfisher plc and B&M, together with construction and infrastructure groups such as Balfour Beatty, Morgan Sindall and Keller Group, are projected to lose less than 10%. That contrast says a lot about where markets may eventually rediscover value once the AI euphoria fades: not in companies promising exponential disruption, but in businesses connected to housing, repairs, logistics, discount retail and the ordinary mechanics of the real economy.