War Has Become a Wealth Transfer From Nations to Balance Sheets

One uncomfortable question keeps coming back whenever I look at modern wars not as a citizen, not as a moral commentator, but as an investor watching the machinery of capital allocation: which of the recent wars has actually improved the life of any nation involved in it? Take Russia’s war against Ukraine. Has life improved for Ukrainians, who live under destruction, mobilization, demographic trauma, debt dependence, and infrastructure damage? Obviously not. Has life improved for ordinary Russians, who face sanctions, isolation, militarization of society, inflationary pressure, lost human capital, and a future increasingly subordinated to the logic of permanent confrontation? Again, no. Even if certain sectors profit, the nation as a living organism does not become healthier, freer, richer, or more secure.

Look at Israel and Gaza. For Gaza, the catastrophe is visible without explanation. But has Israel become a better place to live because of the war? Has the state become more stable, more united, more trusted, more secure, more attractive to capital, more attractive to its own most productive citizens? The answer is hard to defend as “yes.” The same question applies to the confrontation between Israel, the United States, and Iran. Which society became meaningfully better off? Which middle class became safer? Which taxpayer became richer? Which young generation inherited a more predictable future? The answer, again, is almost nowhere. Modern war seems increasingly unable to produce the old promise of national renewal, historical correction, or political rebirth. It produces exhaustion, debt, surveillance, insecurity, fiscal pressure, migration, polarization, and permanent emergency.

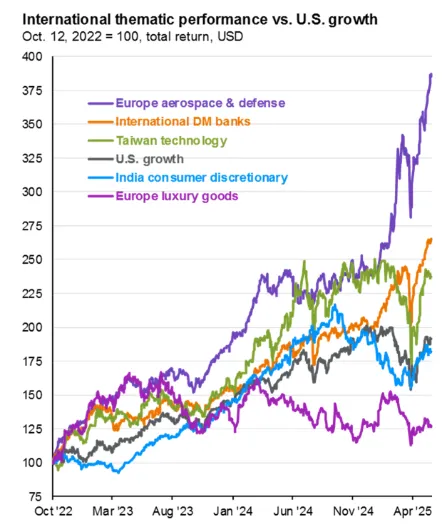

This is where the investor’s view becomes colder than the political view, because markets reveal what official language often hides. If we ask who benefits, the answer is rarely “the nation.” It is rarely the average citizen, the taxpayer, the young family, the soldier, the small business owner, or even the long-term stability of the state itself. The visible beneficiaries are often the industrial and financial structures positioned around the war economy: defense contractors, missile producers, drone manufacturers, ammunition suppliers, cyber-security firms, intelligence contractors, logistics groups, reconstruction intermediaries, commodity traders, energy infrastructure firms, and the financial institutions that fund, hedge, insure, securitize, and distribute the entire process. Look at the equity charts, the order books, the margins, the capitalizations, the political access, and the “strategic importance” suddenly assigned to these companies. Rheinmetall, Leonardo, Thales, Elbit, Hanwha Aerospace, Mitsubishi Heavy Industries, and a broader universe of American, European, Israeli, Korean, and Japanese defense-linked companies do not experience war as tragedy in the same way societies do. For them, war is demand visibility.

The result is still difficult to ignore: modern war increasingly redistributes quality of life away from populations and toward systems that monetize insecurity. The citizen receives taxes, inflation, mobilization, anxiety, censorship pressure, reduced social spending, higher debt burdens, and a permanently degraded sense of future normality. The corporate sector attached to conflict receives contracts, subsidies, urgency, political protection, long-duration procurement pipelines, and a moral vocabulary in which every budget increase becomes “security,” every margin becomes “resilience,” and every industrial expansion becomes “deterrence.”

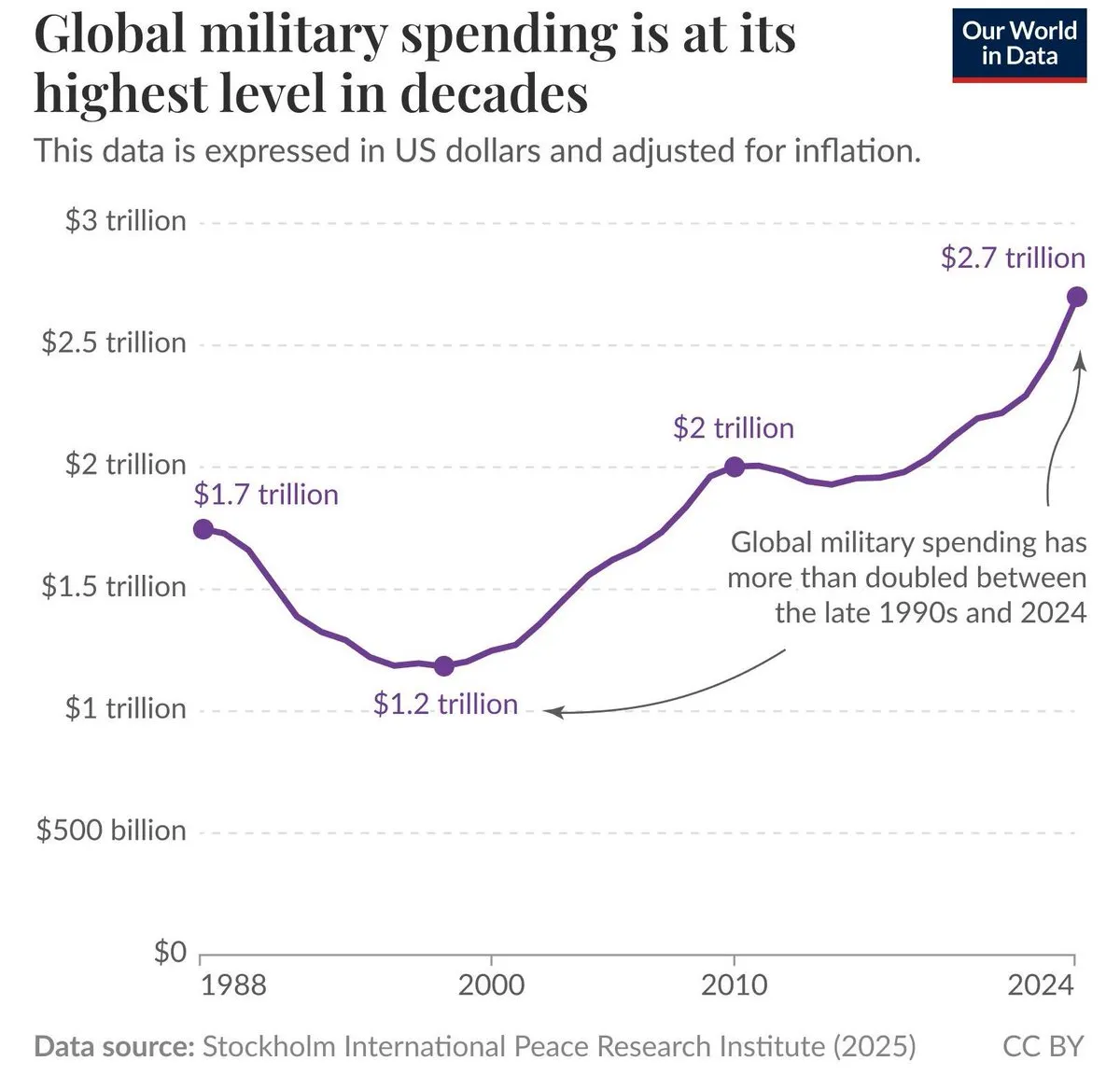

This is what makes today’s wars different from the grand historical narratives many people still carry in their heads. The WWII, despite its almost unimaginable destruction, produced a world in which some defeated and devastated countries eventually rebuilt into more prosperous states. Germany, after catastrophe, occupation, division, guilt, destruction, and defeat, became both West Germany and East Germany, each reconstructed under different systems, and eventually reunified into one of the richest societies on earth. Japan was destroyed and then rebuilt into an industrial power. Western Europe, after being ravaged, was integrated into a new security and economic architecture. The moral price of that history cannot be romanticized, but the postwar order did contain a visible reconstruction logic: institutions, industry, infrastructure, social contracts, currency regimes, and national economies were rebuilt around a promise that ordinary life would become better after the fire.

The disturbing question is whether that logic still exists. In the current era, war often ends less with a Marshall Plan for society than with a procurement cycle for corporations. It does not necessarily produce new constitutional settlements, new social contracts, or broad-based national renewal. It produces frozen conflicts, militarized budgets, sanctioned economies, fragmented trade routes, energy shocks, refugee flows, intelligence expansion, emergency legislation, and a permanent political argument for why civilian priorities must wait. Housing can wait. Healthcare can wait. Education can wait. Infrastructure can wait. Industrial policy cannot wait, once it is attached to missiles, ammunition, drones, satellites, chips, sensors, naval systems, or energy security.

As an investor, I find this morally ugly but analytically important. The market is telling us that the age of “peace dividends” has been replaced by the age of “war dividends,” and those dividends do not accrue evenly to nations. They accrue to sectors. They accrue to balance sheets. They accrue to companies whose products become more necessary as the world becomes more unstable. The paradox is brutal: the worse the geopolitical environment becomes for ordinary life, the better the revenue visibility becomes for parts of the defense-industrial complex. A society may become poorer in real human terms while a defense index makes new highs. A state may become less stable while its contractors become more valuable. A population may become more afraid while investors receive a cleaner earnings story.

So the real thesis goes beyond the obvious destructiveness of modern wars. The real thesis is that modern wars increasingly look like mechanisms through which security anxiety is transformed into corporate cash flow. Political leaders speak the language of national survival, moral duty, deterrence, sovereignty, and historical justice, while capital markets translate the same events into backlog growth, margin expansion, rearmament cycles, energy repricing, insurance premiums, infrastructure spending, and sovereign debt issuance. The nation absorbs the trauma. The taxpayer absorbs the cost. The household absorbs the decline in living standards. The market identifies the suppliers.

That may be the defining macro pattern of our time: war no longer reliably builds states, but it reliably builds industries around the fear that states may fail. And once that becomes the operating model, the most dangerous question is no longer who wins the war, because often nobody truly wins in social terms. The more precise question is who monetizes the permanent preparation for the next one.

Modern war has a strange accounting system: The nation gets debt. The citizen gets inflation. The taxpayer gets the bill. The soldier gets the risk. The household gets a worse future. And the defense contractor gets a higher multiple.

They call it security. Markets call it growth. I call it a new Wealth Transfer.